FHA EAD Submission Portal

FHA EAD Submission Portal Access

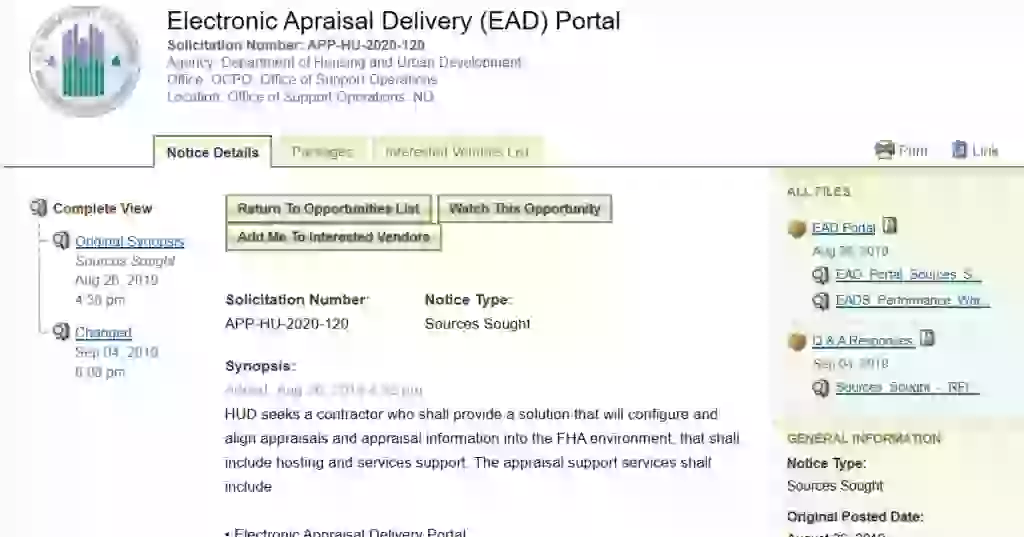

The FHA EAD submission portal is the application for the electronic delivery of appraisals performed through an established set of guidelines (Source). It can be accessed immediately through the link below the page (Source). Submit your appraisals related to FHA mortgage loans, as other submission portals belong to other topics (Source). This step is completed well before the FHA loan requirements are analyzed and before the loan limits for that year are even discussed, because the appraisal is a different step (Source).

When the appraisal is submitted through the aforementioned portal, there is still no FHA loan completed.

It is an exclusively transactional portal for the delivery and access to appraisals submitted for FHA mortgage loans, and not for other loans (Source). This means that in the case of new originations, the EAD users, third-party service providers, appraisers, in general, all authorized users have to submit these appraisals to the FHA only through this portal. This portal, as I indicated, can be accessed directly with the link below.

It is hosted by Veros Real Estate Solutions and it works as a portal for FHA lenders, service providers, and their business partners to submit online their appraisals related to prospective FHA mortgage loans. The FHA EAD has an interface that runs in the background with the FHA insurance systems that are inbound and outbound transmitting information.

All the appraisals, scoring, and other information therein submitted by the aforementioned parties is accessed and retrieved by HUD as required.

How To Access And Login To EAD Portal?

The mortgagees have three methods to access the FHA EAD portal and submit therein the result of the appraise.

- They can access easily through the portal, whose direct link is here below. Once they access they can submit up to ten appraisals at a time. However, the most common practice here of the users is to submit them one by one.

- Users can access through an interface where they can submit hundreds of appraisals at the same time. They can build their own interface following a technical integration guide provided by the FHA.

- The third method is to utilize a service provider who already has an interface released and utilize their interface to access the EAD portal remotely and submit these appraisals. The most known company is probably is Mercury VMP, who owns an appraisal vendor management software and has an interface with the EAD portal.

SAP had also the plan to develop a standard interface from their SAP Real Estate industry solution. However, since 2020 roadmap, this solution was not included.

Access to the portal directly with this link.

Further Readings

We have interesting articles about non-conventional mortgage loans. The basic ones we will recommend to you are stated income loans, where we discuss if they are currently legal or not, how can you obtain one, and the situation of these loans in California. We are also covering other non-conventional mortgages, such as the ITIN mortgages, luxury home financing that is a figure similar to the jumbo loans, the no ratio loans that do not consider the debt-to-income ratio during the underwriting process, and those loans offered by Funding For Flipping.

No doc hard money loans and the very similar hard money construction loans.

If you are into more conventional mortgages such as FHA mortgages, I suggest you read the following related articles described below.

We explain the FHA loan requirements completely, with the current limits for this year. We also go through the appraisal guidelines, and moreover, we are worried about the peeling paint and why it can be an issue.

Completing forms is necessary, so we also study the number format of an FHA case and how to submit an FHA file, how to complete the form HUD 92900, the form for the FHA notice to the homeowner, and the FHA Financing Addendum.

Regarding special housing programs, I would like to include the FHA Back To Work Program.

Furthermore, there are two conflicting situations that can occur that are the situation of a conditional commitment and the identity of interest.

I am David, economist, originally from Britain, and studied in Germany and Canada. I am now living in the United States. I have a house in Ontario, but I actually never go. I wrote some books about sovereign debt, and mortgage loans. I am currently retired and dedicate most of my time to fishing. There were many topics in personal finances that have currently changed and other that I have never published before. So now in Business Finance, I found the opportunity to do so. Please let me know in the comments section which are your thoughts. Thank you and have a happy reading.