FHA Conditional Commitment

FHA Conditional Commitment

In this article, I would like to explain to you the FHA conditional commitment of the prospective buyer and which consequences relevant for can have for you as a homebuyer (Source). An FHA conditional commitment is defined as a notice issued by the FHA lender with the notice for 120 days (Source), of his willingness of financing the mortgage loan if certain FHA loan requirements are met by the prospective homebuyer (Source), such as a credit score, a completed appraisal exercise performed on the property, loan limits for eligibility, and the proof of income.

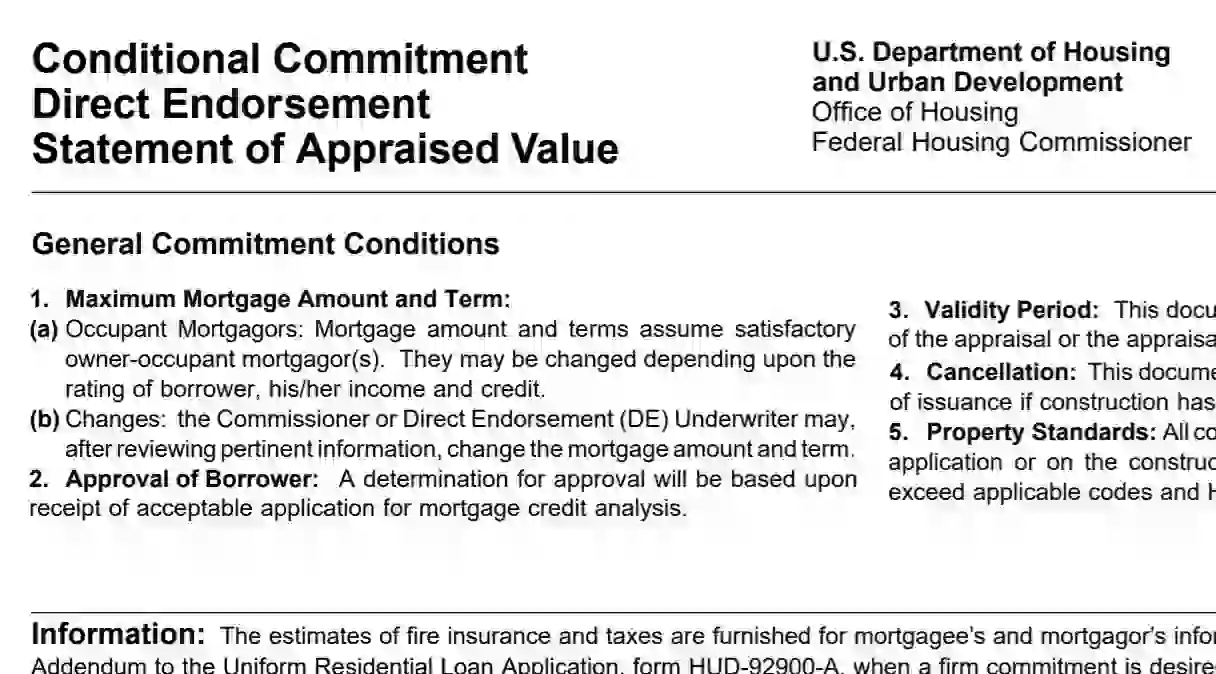

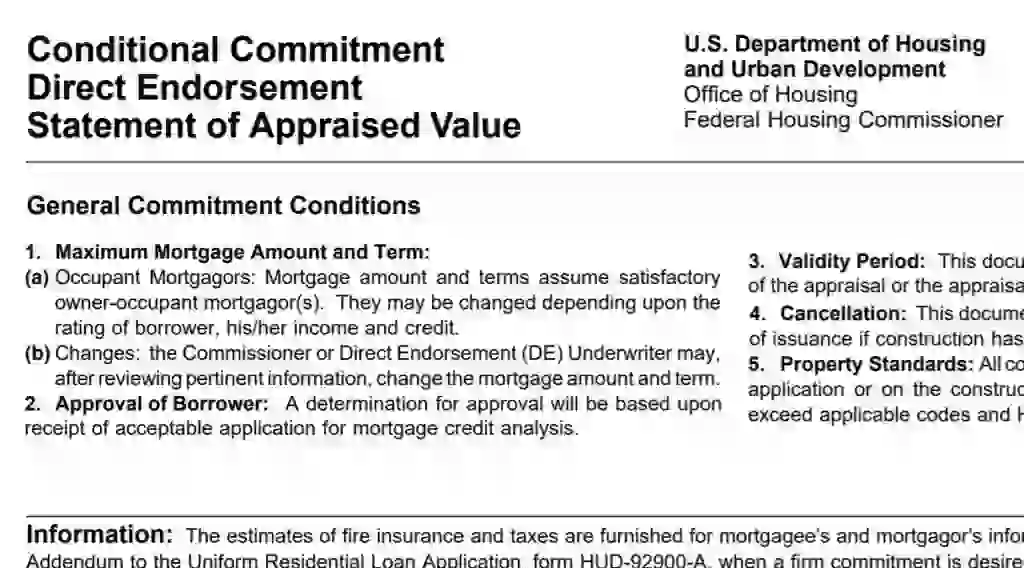

The FHA conditional commitment is a document released by the FHA that states that if the content of the loan application and supporting documents is true and does not change, then the FHA will guarantee the loan. It is a document sent as a letter from the FHA that declares that the FHA will guarantee the loan.

The Federal Housing Administration (FHA) does not make home loans, but guarantees home loans made according to their requirements. Applicants go to an FHA approved mortgage originator and fill out an application. Through the FHA’s system, the originator sends the loan application and supporting documentation to the FHA and receives a conditional commitment which is good for 6 months.

During the FHA loan process, there is a step to execute that is the FHA appraisal process. When this process is performed, the participants (borrower and FHA lender) understand the fair market value and the general condition of the real estate object.

Now the next step in the FHA loan process, is that the prospective buyer, the borrower, is enabled to offer to the seller and FHA lender, a commitment to acquire the property.

The borrower can offer this commitment to the other parties, or he can dismiss the overall operation and do not purchase the property through the FHA mortgage loan.

What happens if the buyer does not exercise this commitment for some time? What happens with the validity of the appraisal after some time? If the appraisal expired, should the parties arrange with the appraiser for a new FHA appraisal? Let´s see the answers and how to proceed.

FHA appraisals cannot be valid forever, because there are situations in the market that make properties to change their fair market value. They are considered released when they are transmitted through the FHA EAD portal manually, or through a service provider.

Therefore, the FHA offers options to the buyer who for whatever reason delayed in the commitment to the acquisition of the property.

In the case of existing properties, if the contract to purchase the property is signed or the borrower has the FHA mortgage loan approved before the expiration date of the appraisal, the validity of the existing FHA appraisal can be extended by the FHA lender for thirty days in order to permit the closing of the FHA loan. Therefore, the answer is yes: When these aforementioned circumstances are met, the prospective buyer may have the benefit of an extension of the FHA conditional commitment.

IF THE CONTRACT TO PURCHASE THE PROPERTY IS SIGNED OR THE BORROWER HAS THE FHA MORTGAGE LOAN APPROVED BEFORE THE EXPIRATION DATE OF THE APPRAISAL, THE VALIDITY OF THE EXISTING FHA APPRAISAL CAN BE EXTENDED BY THE FHA LENDER FOR THIRTY DAYS IN ORDER TO PERMIT THE CLOSING OF THE FHA LOAN.

Likewise, there are other additional requirements. When the borrower successfully underwent the approval process and the signature of the form HUD-92900-LT is completed, the FHA loan process “must close within 150 days”.

These 150 days, in accordance always to the FHA, are disaggregated encompassing “120 day validity period for the original report plus thirty-day extension” in cases where an FHA appraisal has not been “updated with an Appraisal Update Report”.

On the other hand, in situations where there is an update of the FHA appraisal, the FHA loan should close within two hundred and forty days, which again the FHA disaggregates including a “120 day validity period plus 120 day validity period for the Appraisal Update Report.”

Elimination Of The Market Conditions Addendum Form

The requirement for FHA appraisers to include the Market Conditions Addendum was suppressed at the end of 2018. This was the 1004MC form. This addendum was an attachment to the appraisal.

Some time ago in 2020, Freddie Mac broadcasted an important clarification, stating that the scope, volume, and quality of work expected for the appraiser has been simplified eliminating this form, but he is still obliged to study the market conditions and analyze location and neighborhood.

Finally, if you have a concern regarding the fact that the FHA appraisal expires before the closing of the loan, ask your FHA lender what needs to be done to request an extension considering the regulations we described in this article.

Further Readings

We have interesting articles about non-conventional mortgage loans. The basic ones we will recommend to you are stated income loans, where we discuss if they are currently legal or not, how can you obtain one, and the situation of these loans in California. We are also covering other non-conventional mortgages, such as the ITIN mortgages, luxury home financing that is a figure similar to the jumbo loans, the no ratio loans that do not consider the debt-to-income ratio during the underwriting process, and those loans offered by Funding For Flipping.

No doc hard money loans and the very similar hard money construction loans.

If you are into more conventional mortgages such as FHA mortgages, I suggest you read the following related articles described below.

We explain the FHA loan requirements completely, with the current limits for this year. We also go through the appraisal guidelines, and moreover, we are worried about the peeling paint and why it can be an issue.

Completing forms is necessary, so we also study the number format of an FHA case and how to submit an FHA file, how to complete the form HUD 92900, the form for the FHA notice to the homeowner, and the FHA Financing Addendum.

Regarding special housing programs, I would like to include the FHA Back To Work Program.

Furthermore, there are two conflicting situations that can occur that are the situation of a conditional commitment and the identity of interest.

I am David, economist, originally from Britain, and studied in Germany and Canada. I am now living in the United States. I have a house in Ontario, but I actually never go. I wrote some books about sovereign debt, and mortgage loans. I am currently retired and dedicate most of my time to fishing. There were many topics in personal finances that have currently changed and other that I have never published before. So now in Business Finance, I found the opportunity to do so. Please let me know in the comments section which are your thoughts. Thank you and have a happy reading.