FHA Notice To Homeowner

FHA Notice To Homeowner: The HUD 92210-1 Form

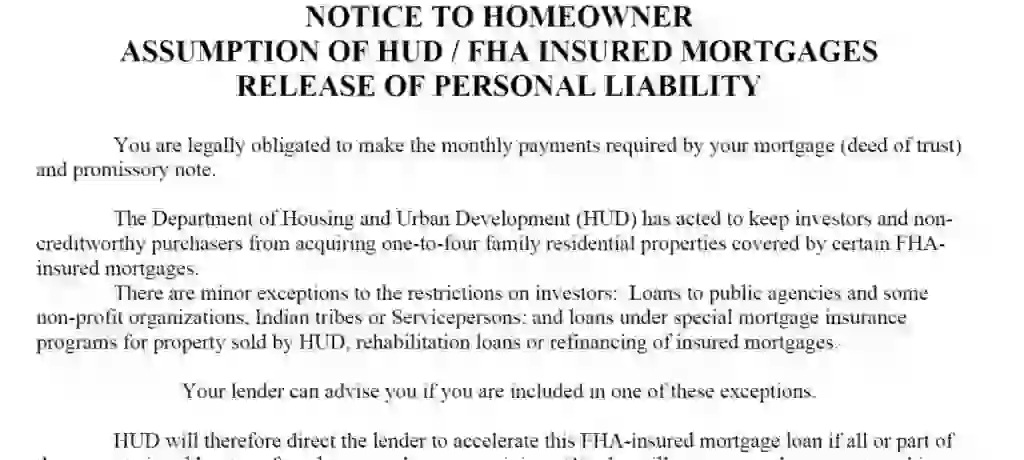

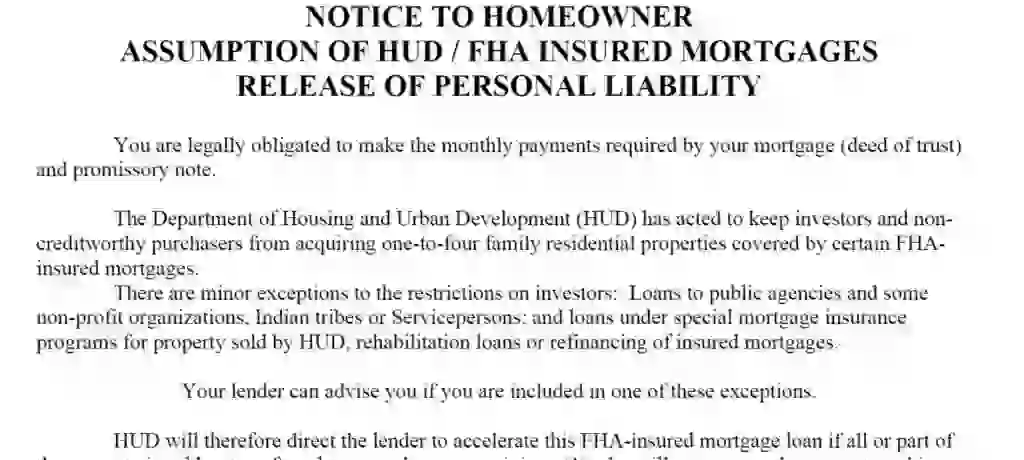

The FHA notice to homeowner of the assumption of FHA / HUD-insured mortgages (Housing and Urban Development Administration in the federal government) is a formal notification (Source) that he has the legal obligation to perform each month the payment obliged by his mortgage contract and promissory note (Source).

THE FHA NOTICE TO HOMEOWNER IS A FORMAL NOTIFICATION THAT HE HAS THE LEGAL OBLIGATION TO PERFORM EACH MONTH THE PAYMENT OBLIGED BY HIS MORTGAGE CONTRACT AND PROMISSORY NOTE

If he sells his property by allowing the purchaser the assumption of the payment for the mortgage through an agreement in the contract, he is nevertheless still legally assuming the liability for the original mortgage signed (Source). This obligation continues, except that he obtains a release from the original liability from the previous lender of the mortgage loan contract (Source).

For this, obviously, there is already an FHA mortgage in place, for which the buyer had to fulfill the FHA loan requirements and within the loan limits for the year where the FHA mortgage was agreed. (Source) These principles apply to other types of obligations as well (Source)

FHA NOTICE TO HOMEOWNER

FHA NOTICE TO HOMEOWNER

STEP BY STEP WHAT TO DO:

This release of the original liability can be obtained, and here is where the form HUD 92210-1 and the FHA notice to homeowner come into play:

- Performing the release request in a written document.

- Having the credit of your buyer in complete approval by the lender or the FHA / HUD.

- Performing the request that the buyer of your real estate object executes a contract where he agrees on the assumption and subsequent payment of the debt arising from the mortgage agreeing as a consequence, to become the substitute mortgagor.

- That finally the lender completed the Form HUD 92210-1 “Approval of Buyer and Release of The Seller.”

If you, still obliged by the mortgage, become the seller of the home afterwards and do not receive from the lender any release from the original contractual liability and even if the buyer is assuming the responsibility for the mortgage debt, then the buyer of the home and you (as you were never released) both will be liable for the payment. This liability is a joint liability and also an individual liability for any kind of default of five years after the date that this was assumed.

After these aforementioned five years, only the buyer will continue to be liable, except when the mortgage is in default at the moment the five year period comes to expiration.

In the case that the buyer decides to take the title subject to the mortgage without the assumption of personal liability for this obligation, you will continue in liability for the complete term of the mortgage loan.

The conclusion now is that if anyway you desire to become released from this contractual liability, the only subject who can release you is the lender of the mortgage. Therefore, you should contact the mortgage lender and obtain a release of the liability from him.

IF ANYWAY YOU DESIRE TO BECOME RELEASED FROM THIS CONTRACTUAL LIABILITY, THE ONLY SUBJECT WHO CAN RELEASE YOU IS THE LENDER OF THE MORTGAGE. THEREFORE, YOU SHOULD CONTACT THE MORTGAGE LENDER AND OBTAIN A RELEASE OF THE LIABILITY FROM HIM.

The mortgage lender or FHA mortgage lender does not have any reason to release you, in principle, as he would prefer to have to subjects obliged, individually and jointly, for the payment.

Therefore, address the mortgage lender for any question related to becoming released from the original liability, and for other questions simply address the local office of the HUD. It is also the lender who can help you provide the address of the competent HUD office. This HUD office will be the one who has jurisdiction over the home.

I hope that the subject of the FHA notice to the homeowner is now clear and basically it is related to the assumption of the obligations for the original mortgage loan and which of the subjects remain, jointly and individually, liable afterwards. You can download here a sample of the HUD 92210-1 form that was described here.

Further Readings

We have interesting articles about non-conventional mortgage loans. The basic ones we will recommend to you are stated income loans, where we discuss if they are currently legal or not, how can you obtain one, and the situation of these loans in California. We are also covering other non-conventional mortgages, such as the ITIN mortgages, luxury home financing that is a figure similar to the jumbo loans, the no ratio loans that do not consider the debt-to-income ratio during the underwriting process, and those loans offered by Funding For Flipping.

No doc hard money loans and the very similar hard money construction loans.

If you are into more conventional mortgages such as FHA mortgages, I suggest you read the following related articles described below.

We explain the FHA loan requirements completely, with the current limits for this year. We also go through the appraisal guidelines, and moreover, we are worried about the peeling paint and why it can be an issue.

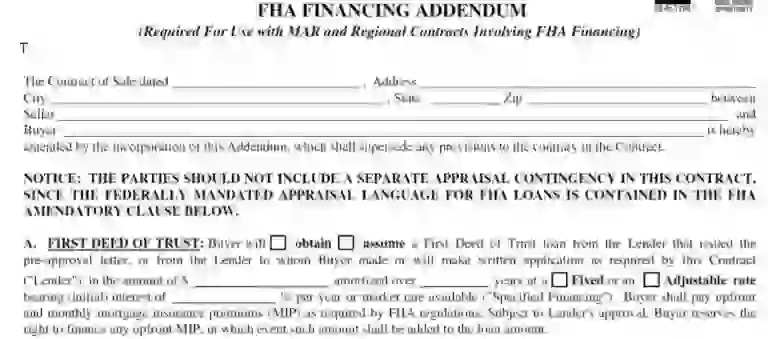

Completing forms is necessary, so we also study the number format of an FHA case and how to submit an FHA file, how to complete the form HUD 92900, the form for the FHA notice to the homeowner, and the FHA Financing Addendum.

Regarding special housing programs, I would like to include the FHA Back To Work Program.

Furthermore, there are two conflicting situations that can occur that are the situation of a conditional commitment and the identity of interest.

I am David, economist, originally from Britain, and studied in Germany and Canada. I am now living in the United States. I have a house in Ontario, but I actually never go. I wrote some books about sovereign debt, and mortgage loans. I am currently retired and dedicate most of my time to fishing. There were many topics in personal finances that have currently changed and other that I have never published before. So now in Business Finance, I found the opportunity to do so. Please let me know in the comments section which are your thoughts. Thank you and have a happy reading.

A home loan limit is essentially the maximum amount of money you can borrow from an approved lender to purchase a property. The spacious home you imagined in your mind with all its amenities comes at a price you must qualify for with your VA Loan Specialist. Conventional loans, FHA loans, and other home loans have loan limits, but only VA Home Loans have you and your military family in mind.