Residential Whole Loan

Residential Whole Loan

A residential whole loan is an individual loan issued to a borrowing party where the object is real estate with residential purposes (1) (3) excluding commercial loans and rural developments (4). Originators of residential whole loans frequently resell these loans through the aftermarket to brokerages (5), financial institutions, and government agencies (7) in order to mitigate their risk assumptions (6) (8). Rather than holding a loan within their balance sheets for ten or twenty years, the lending party is able to recover the principal nearly instantaneously by reselling the entire loan, the residential whole loan, to an institutional buyer, such as Fannie Mae and Freddie Mac (2) (9) (10).

A Residential whole loan is a type of “whole loan” referred to as mortgage loans for real estate objects with residential purposes. A residential whole loan is the complete mortgage loan issued to the borrower. It is opposed to a securitization, where several financial assets are merged or pooled to form a complete package and therefore, are not “whole” loans.

Residential whole loans can be issued for a number of reasons, but they always include the purchase of real estate for residential purposes. Whole loans for business equipment or working capital enter into a different category.

A lending entity can extend a mortgage loan to a debtor with specific stipulations established by the lender after an underwriting procedure. As a rule, residential whole loans are maintained on a credit issuer’s financial statement and the debt issuer bears responsibility for servicing the loan.

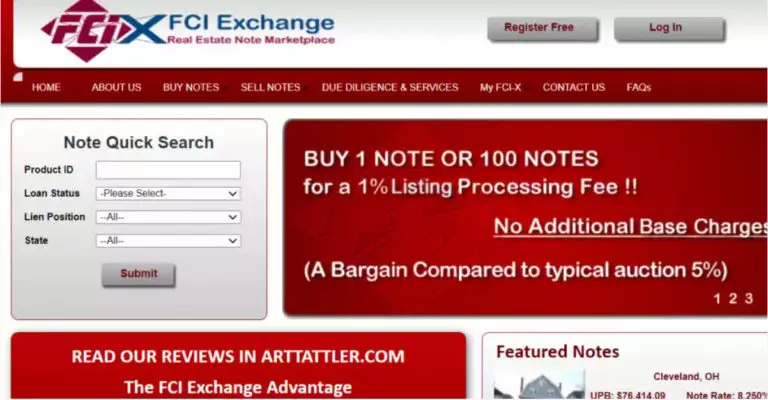

So what can the credit issuer do with those residential whole loans? Well, the lender has the secondary mortgage market to negotiate this whole loan.

The secondary market is an active marketplace where banks and other lenders trade their loans with large financial institutions. It’s a liquid place for trading because of the many buyers looking to purchase different types of residential whole loans from various sources like Freddie Mac or Fannie Mae, which are agencies that act as wholesalers for mortgages in this arena.

Securitization takes these packages of individual entire mortgages (or “residential whole loans”) and sells them off in smaller chunks all around the market. So the process of securitization involves the pooling, merging, or disaggregation of these whole loans.

Banks and other lenders that want to reduce their risks may want to consider selling residential whole loans. Whole loan sales are an attractive alternative for securitization because they can help the lender earn money from origination fees, sell off assets and still receive cash flow immediately, at a discounted price, as opposed to waiting months or years (normally years in the case of residential whole loans because these are mortgage loans) until credit issuers get paid back by the debtors who have taken out mortgage loans.

The secondary market entities will likely require that these whole-loan sellers meet specific underwriting criteria before transactions go through. So here, non-conformance loans are out of the question. If the originator does not follow adequate underwriting criteria, the secondary market will reject this loan and the credit issuer will have to keep it.

Most investors are aware of the benefits of investing in real estate. It is investing in a tangible asset with ongoing cash flow, where values usually increase and that have tax advantages that are not available in other types of assets.

Investing In These Assets

There is actually a lot that goes into pulling off successful real estate investments: inspections, mortgage applications, coordination, property upgrades, dealing with tenants, and the list goes on and on.

These problems are typical issues of the lender. There is, nevertheless, a better way to invest in these cases. Here is how it works.

Banks, hedge funds, and other financial institutions actually sell residential whole loans, in the form of mortgages to smaller groups of investors. There is a variety of different products available to invest in based on your risk appetite but the most exciting returns are in mortgage loans that are in need of specialized servicing.

These residential whole loans can be purchased for thirty to forty percent of their face value because borrowers have stopped paying or are in a high-risk category.

This particular situation in the borrower provides smaller investors the flexibility to do what the banks cannot do or will not do according to their internal policies and risk protocols.

So there are financial institutions that have partnerships in place to work with homeowners, not only to avoid foreclosure but also to provide improved credit benefiting families.

For the investor, it is also a big benefit because superior returns can be retrieved and enjoying the benefits associated with owning real estate without most of the headaches and receive high yields secured by real estate property.