Gold IRA Tax Rules

Gold IRA Tax Rules

We do here a thorough analysis of the gold IRA tax rules. in our complete guide about what is gold IRA, we only summarized a few bullet points.

The tax treatment is one of the several benefits of gold IRA, and we explained all of them in that article.

The Internal Revenue Service allows certain types of precious metals – gold, silver, platinum and palladium — to be purchased by an individual retirement account. A Gold IRA is a generic term for a self-directed IRA that holds any of the four acceptable precious metals.

When an IRA is self-directed, the custodian has wide latitude to hold various types of assets in the account. Gold IRAs are usually set up with precious metal broker/dealers who can buy, sell and store your physical coins and bars.

In order to be compliant with gold IRA tax rules, you must limit your precious metal purchases to coins and bars acceptable to the IRS. Otherwise, you will be subject to an excise tax and your IRA may lose its status as an IRA.

Normally, the precious metal must be 99.9 percent pure, although certain exceptions exist for specific coins. The only kind of coins allowed are bullion and some proofs– you can’t use your IRA to collect rare numismatic coins.

If you’re part of the 32% of working Americans with a workplace retirement account, congratulations! You’re already steps ahead of many other Americans, two thirds of whom don’t contribute anything to a 401(k) or other retirement account available through their employer, according to Bloomberg.

You can get even further ahead, all while potentially mitigating more risk. In addition to contributing to an employer-sponsored 401(k), you can contribute to a Roth IRA, traditional IRA, or a traditional or Roth self-directed IRA.

If you don’t exceed the maximum contribution limits (based on your income level and age), you can contribute to all of your retirement accounts throughout the tax year. You may consider consulting your tax advisor to determine your eligibility.

“Because gold prices generally move in the opposite direction of paper assets, adding a gold IRA to a retirement portfolio provides an insurance policy against inflation,” says Edmund C. Moy, former United States Mint Director and U.S. Money Reserve Senior IRA Strategist. “This balanced approach smooths out risk, especially over the long term.”

Several different forms of gold and other precious metals are acceptable, including:

Gold

American Gold Buffalo uncirculated coins (proofs not allowed)American Gold Eagle bullion coinsAmerican Gold Eagle proof coinsAustralian Kangaroo/Nugget coinsAustrian Gold Philharmonic coinsCanadian Gold Maple Leaf coinsChinese Gold Panda coinsGold rounds and bars produced by a COMEX- or NYMEX -approved national government mint or refinery, meeting minimum fineness requirements

Silver

American Silver Eagle bullion coinsAmerican Silver Eagle proof coinsAustralian Silver Kookaburra coinsAustrian Silver Philharmonic coinsCanadian Silver Maple Leaf coinsChinese Silver Panda coinsMexican Libertad coinsSilver rounds and bars produced by a COMEX- or NYMEX -approved national government mint or refinery, meeting minimum fineness requirements

Platinum

American Platinum Eagle coins American Platinum Eagle proof coins Australian Platinum Koala coins Canadian Platinum Maple Leaf coins Isle of Man Noble coins Platinum rounds and bars produced by a COMEX- or NYMEX -approved national government mint or refinery, meeting minimum fineness requirements

Palladium

Canadian Palladium Maple Leaf coinsPalladium rounds and bars produced by a COMEX- or NYMEX -approved national government mint or refinery, meeting minimum fineness requirements.

Withdrawal Gold IRA Tax Rules

Traditional IRAs

Traditional IRA contributions are tax-deductible. However, you must pay taxes when you withdraw money or precious metals from your traditional IRA.

The amount you withdraw is added to your annual gross income and is subject to ordinary income tax (not capital gains tax). You must also pay a 10 percent early withdrawal penalty for distributions you take before age 59 ½.

However, you can avoid the penalty under certain circumstances, such as using the money to purchase your first home or to pay for medical insurance when you are unemployed.

You can also avoid the penalty by setting up an annuity based upon your life expectancy. You must begin taking distributions by age 70 ½ or else face a 50 percent excise tax on the amount you failed to withdraw each year.

Roth IRAs

Roth IRA contributions, though not deductible, are always tax-free when withdrawn. Earnings are subject to taxation and penalties under two circumstances:

- The account is less than five years old

- You are under age 59 ½

The first condition always applies, regardless of age. The penalty arising from the second condition can be waived by the same sort of exceptions that apply to traditional IRAs. All other Roth IRA distributions are tax- and penalty-free. Unlike traditional IRAs, Roth IRAs do not require minimum distributions at age 70 ½ or any other age.

Bequests

You avoid all taxes and penalties on your remaining IRA balance when you die. Your beneficiaries will have to pay taxes on the money or precious metals they withdraw from an inherited traditional IRA, although inherited Roth IRAs are tax-free.

The 10 percent penalty is waived if you inherit an IRA from someone who dies before age 59 ½. However, the 5-year rule for Roth IRAs still applies.

Normally, you can space out withdrawals from an inherited IRA to reduce the annual tax bite. You always are entitled to a five-year span, and may qualify for a much longer withdrawal period depending on several factors, including:

- Your relationship to the deceased

- Your age

- The age of the oldest beneficiary

- The deceased’s age at the time of death

- Whether any of the beneficiaries is some entity other than an individual, such as a charity or trust.

You can cash in your precious metals before withdrawing them, or can withdraw them directly. In the latter case, the tax is determined by the current fair-market value of the precious metal.

How Does A Gold IRA Work

Gold IRA is not just about better tax rules. There are many Gold IRA rules to take care of. Let´s see how it all works.

Use a Self-Directed IRA

A self-directed IRA is a retirement plan that lets you make alternative investments to build wealth and diversify your portfolio. Instead of being limited to stocks, bonds, and other similar assets, you can invest in assets like real estate and precious metals. You need to set up a self-directed IRA account if you want to purchase gold and other precious metals. Traditional self-directed IRAs offer tax-deductible contributions, with withdrawals taxed as ordinary income.

You can use your self-directed IRA to purchase precious metals like gold, silver, platinum, and palladium. Moreover, there are certain rules you must follow to ensure your IRA investments are in line with IRS rules and regulations.

Choose IRA-Eligible Gold

Certain prerequisites for gold coins and bullion apply when determining what to put in a self-directed IRA. Your IRA provider can guide you about specific coins, bars, and bullion options. The following are the requirements established by the IRS:

- At least 99.5% pure.

- Coins that the US government mints including gold coins like the American Eagle and Buffalo gold coins and silver ones like the American Eagle and Silver Eagle.

- Comes from a reputable dealer registered with the US. Treasury, so your money is protected in case something goes wrong.

- An IRA custodian must store it in an approved depository.

- Credit Suisse gold bars manufactured at an approved facility.

- Silver bars & coins must be 99.9% pure.

- Palladium and Platinum bars and coins must be 99.95% pure.

The IRS purity requirements ensure that investors are purchasing high-quality metals that will protect their wealth for generations to come.

The IRS sometimes considers IRA-eligible gold to be collectible if it has been certified by an independent organization, such as the Professional Coin Grading Service. Unfortunately, this means you can’t hold it in your gold IRA. Therefore, if you want to have your gold and other precious metals professionally graded, you should wait until after you have liquidated and possess your IRA assets.

Purchase Your Gold through a Custodian

In order to include precious metals in your IRA, it is necessary to collaborate with impartial trustees or Gold IRA custodians who are capable of storing and overseeing your metals. By purchasing gold through a precious metals IRA custodian, you can be confident that your assets are being safeguarded in compliance with federal regulations.

Custodians offer a simple and convenient way to own physical precious metal assets. Your custodian will help you set up an account and buy gold and other precious metal assets. They will also handle the transfer of funds from your bank to the dealer, loosen the purchase of physical precious metals, and safely store your assets in a depository outside your local jurisdiction.

Because gold IRA companies generally work with top-tier custodians, they offer these services as part of a comprehensive service package. As a result, most gold IRA investors purchase gold and other precious metals with funds already in their accounts. The following are some ways to fund your IRA account:

- Cash contributions to your account of up to $5,000 per year.

- Rollovers from other retirement plans. You can roll over an existing IRA or 401(k) plan into a gold IRA.

- Transfer existing assets from a self-directed IRA to a new self-directed gold IRA account.

It’s essential to choose a gold IRA custodian that is properly licensed and insured, has a reputation for integrity, and follows all industry regulations when handling your assets. When selecting a gold IRA custodian, consider the following:

- Is the company USA regulated?

- Are there any restrictions on products offered by the custodian?

- What fees does the custodian charge?

- How long has the custodian been in business?

- Is the custodian audited by an independent firm?

- Does it have a good reputation among consumers and regulators?

- Does it have an amicable customer service team?

Store Your Gold in an IRS-Approved Depository

You must keep your precious metals in an IRS-approved storage facility if you own a gold IRA. The IRS does not permit you to store coins and bars at home or in a safety deposit box. Many people mistakenly assume they can simply hand their gold and precious metals over to a family member or friend with favorable tax implications.

If you possess the IRA-eligible gold and precious metals even for a brief period, the IRS will consider it a distribution. This would result in you paying heavy taxes and penalties.

To ensure your gold is safe, your IRA custodian will transfer your physical metals to a secure storage facility called a depository. You may choose the depository, or your custodian can recommend one. It is vital that the depository is IRS-approved.

When choosing a depository, consider its security measures, insurance policies and storage fees. You can store it in a depository and hold it until you request the sale of your gold through a custodian. A secure delivery service will then take your gold to your home address.

So, to summarize this important paragraph.

You can’t keep IRA-eligible gold in your home or in a local security deposit box.

Eligible gold can be included in your IRA “provided it is in the physical possession of a bank or an IRS-approved nonbank trustee,” according to the IRS.

Storing your IRA gold at home can be considered as taking a distribution, which means you may lose your tax-deferred benefits and could get hit with a penalty if you’re under 59½ years old. What’s more, if the IRS determines that the day your IRA gold entered your home was the date of “distribution,” you may end up paying additional penalties and back taxes owed from the time of distribution.

“The IRS,” writes The Wall Street Journal, “warns taxpayers to be wary of anyone claiming that precious metals held in your IRA can be stored at home or in a safe-deposit box.”

Segregated vs Allocated Storage

There are two main forms of precious metals storage: segregated and allocated. While both are secure, you may prefer one over the other depending on your unique financial situation.

Segregated storage is a form of storage in which your assets are held separately from other gold or silver assets that are either owned outside of the IRA or owned by other people. This may be preferable if you want easy access to your precious metals for the sake of liquidity.

Allocated storage (also known as commingled storage) is where your precious metals assets in your IRA are stored along with other precious metals owned by multiple account holders. Though your precious metals are still properly labeled and attributed to you, this storage method may be better if you don’t need quick access to them.

Hold the gold in your IRA until you are 59 ½

Precious metal IRAs are designed to hold gold, silver and other precious metals until you retire. With a precious metal IRA, you can defer taxes on your profits and take advantage of tax-deferred compounding growth. However, there are restrictions on when you can withdraw your IRA assets.

Following IRS regulations, distributions from a gold IRA plan must be deferred until the account owner reaches the age of 59½. At that time, you will be subject to any taxes due on the amount of your withdrawal. Only then can the metals in the account be liquidated for cash or possession without penalty.

When you invest in a gold IRA, your capital is invested in physical gold and precious metals. You can hold onto and sell them later, use them as a hedge against economic or geopolitical crises, or pass them on to the next generation. Keep in mind that if you withdraw funds from your retirement savings before the age of 59½, you must pay a 10% early withdrawal penalty and a 28% capital gains tax on any profits.

There are several exceptions to paying the 10% penalty on early withdrawals, including if an individual becomes disabled or buys a first home. A penalty can also be avoided if payments are made in the form of an annuity based on one’s life expectancy.

At age 72, you must begin taking mandatory distributions from your gold IRA. If you don’t, you will face a 50% excise tax each year that you do not meet the distribution requirements.

Once you are 59½ years old, you can liquidate the precious metals in your self-directed IRA without penalty for cash or take possession of your physical precious metals. The latter option is known as a “distribution in kind.”

Unlike withdrawing funds from a traditional retirement account, withdrawing from a precious metals IRA allows you to walk away with a powerful physical asset in hand—gold (or other precious metals)—which you can hold onto, sell at a later point, use as currency in a time of crisis, or pass down to future generations.

Limits to the contribution

Avoid contributing more than you can. The IRS sets annual contribution limits for individual retirement accounts each year. Moreover, you can contribute up to $6,000 or $7,000 per year to an IRA if you are over 50 years.

XXXX

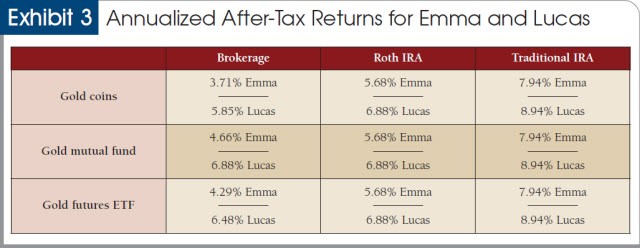

Like all IRA investments, gains from gold sold within an IRA are not taxed until cash is distributed to the taxpayer, and distributions are taxed at the taxpayer’s marginal tax rate. To illustrate the tax consequences of owning gold, Emma, a wealthy taxpayer, and Lucas, a median income taxpayer, provide an example.

Example. Emma is 60 years old and single and has $398,500 in annual taxable income. She is considering one of three options to invest $10,000 in gold: U.S. gold coins, a gold mutual fund, or a gold futures ETF. She is also considering whether to make her investment through a brokerage account, a Roth IRA, or a traditional IRA. Emma plans to hold the investment for 10 years, when her marginal tax rate will be 28% (and her modified adjusted gross income (MAGI) will be below the threshold amount for application of the net investment income tax under Sec. 1411(b)), and then sell, and in the case of the IRAs, distribute the proceeds.

Lucas is 60 years old and single and has $60,000 in annual taxable income. After retirement, he expects his taxable income to fall to within the 15% marginal rate on ordinary income. Lucas is considering the same gold investment choices as Emma and has the same plans for selling and distributing any proceeds. Exhibit 2 provides comparative information for Emma and Lucas.

For comparability, the before-tax contribution to the regular IRA is $10,000, while the contributions to the brokerage account and the Roth IRA are with after-tax dollars—$6,700 for Emma and $7,500 for Lucas.

The results for Emma and Lucas, shown in Exhibit 3, indicate that the after-tax returns of gold investments in a traditional IRA dramatically exceed those of gold investments in a brokerage account or a Roth IRA. Lucas’s annualized after-tax return increases by more than two percentage points by using a traditional IRA for his gold mutual fund investment and more than three percentage points over a brokerage account by using a traditional IRA for his investment in gold coins. For Emma, the results are even more dramatic. She gains more than 3.2 percentage points of annualized after-tax return by using a traditional IRA instead of a brokerage account for her gold mutual fund investment and more than 4.2 percentage points of annualized after-tax return for her investment in gold coins.

The 3.8% net investment income tax may apply to gains on gold from the brokerage account for taxpayers with higher MAGIs than in these examples. However, under Sec. 1411(c)(5), net investment income does not include distributions from a Roth or traditional IRA (or other specified qualified plans)—another reason for higher-income taxpayers to favor an IRA as a gold investment vehicle.

It is also important to note the differences in after-tax returns between the gold investment types held in a brokerage account. The annualized after-tax return on the gold coins is the lowest—about a percentage point lower than the gold mutual fund, which receives LTCG treatment. The example assumes that the costs and fees for buying, owning, and selling gold coins, gold mutual funds, and gold futures ETFs are the same. However, the total costs of owning gold vary widely among investment types and reduce after-tax returns. When buying gold, taxpayers should carefully compare annual costs, including annual maintenance fees, storage charges, buying costs, and selling costs, before selecting the investment.

Brightening gold’s luster

When gold increases in value and provides gains, robust before-tax returns might not translate into robust after-tax returns. Purchasing physical gold coins, bullion, or ETFs provides direct exposure to gold, but the collectibles tax treatment imposes a much higher tax rate. With some planning, investors can keep more of their gold returns by investing in gold that receives LTCG treatment or by placing the investment in an IRA. While secondary gold investments such as gold mining stocks, mutual funds, ETFs, or ETNs may yield lower before-tax returns, the after-tax returns may be more attractive. Alternatively, a physical gold CEF is a direct gold investment but has the benefit of taxation at LTCG rates.

While gold remains a popular investment, recent price declines have diminished the shine. The focus of this article has been on gains, but investors should also consider the consequences of a loss. Gold and all collectibles have the ultimate disadvantage of gains being taxed at the higher collectibles tax rate, with losses being first used to offset capital gains, which may be taxed at the lower LTCG rates. An individual taxpayer’s mix of investment gains and losses, risk profile, and success in investing ultimately determines the results, but a little tax planning can certainly increase gold’s luster.

EXECUTIVE SUMMARY

After-tax returns on gold held as a long-term investment depend on, among other things, whether gains are subject to long-term capital gains tax treatment or are subject to the higher maximum collectibles rate. The latter applies generally to physical gold, such as coins and bullion. Purchases of physical gold may also entail storage and insurance costs.

Most gold investments can be held in an individual retirement account (IRA), which can increase after-tax returns significantly. Trustees of an IRA investing in gold may charge flat fees for storage and administration.

Whether through a brokerage account or via a Roth or traditional IRA, individuals may also invest in gold indirectly through a variety of funds, gold mining corporation stocks, and other vehicles, including exchange-traded funds (ETFs) and exchange-traded notes. Gains from stocks, mutual funds, and gold mining ETFs held more than one year are taxed as long-term capital gains.

Comparisons of hypothetical taxpayers generally indicate a significantly higher after-tax rate of return for any form of gold held in a traditional IRA than in a brokerage account and slightly higher than in a Roth IRA. For brokerage accounts, a gold mutual fund investment may be more likely to provide a higher after-tax return than gold coins or a gold futures ETF.

Taxes on Distributions

Gold IRA accounts are held by a bank or precious metal broker. Taxes on gold ira distributions are calculated based on the fair market value of the metals.

While taxes on gold ira distributions are often overlooked, they are very important to consider for investors. Although they are inevitable, annual returns can help you maximize your after-tax return.

While traditional gold IRAs are tax-deferred, the gains that occur from any sales are still subject to taxes. These taxes can be applied and are applied once you have drawn the funds from your gold IRA.

However, you may be eligible for a tax deduction if you contribute to your gold IRA. Even if you are a high-income taxpayer, you may be charged more than 20% collectible rates of tax. These rates are different for everyone so it’s worth consulting with your tax advisor before withdrawing funds.

When you take out gold from your gold IRA you must be sure that you are having a metal , purchasing that is 99.9% pure. Otherwise you risk losing your IRA status. The only exception to this rule are nuance gold coins, and platinum bars. If you do not follow these rules, you can lose the tax-deductible status of your gold IRA.

And do not forget that your traditional IRA contributions are tax-deductible.

Early Withdrawal Penalties

IRA owners have 10% early withdrawal penalties if they start their mandatory distributions before they reach the age of 70 and a half years old.

There are many exceptions to this rule.

One exception is if a person becomes hospitalized or becomes unemployed. Another exception is if the person engages in substantially equal periodic payments of the same amount of gold or other precious metal.

The IRS will still levy an early withdrawal penalty though. So keep that in mind.

Although gold is relatively a safe investment, it is important to understand the risk associated with this asset. It does fluctuate and therefore it is not risk-free.

The price of gold can also drop or rise and physical assets can be stolen. While most custodians ensure that their assets are protected, theft can happen.

In addition, early withdrawal penalties can make gold IRAs unattractive to investors. To avoid paying an early withdrawal penalty, consider using an IRA with a gold component.

These plans may allow you to buy physical gold and sell it later. You can use that cash for emergencies or pass it to your heirs.

The early withdrawal penalties for gold IRAs are generally 10%. But certain situations qualify for exemptions: disabled Americans or even individuals, first-time homeowners. Also, annual payments will not have to pay an early withdrawal penalty.

Another exception to the early withdrawal penalty for gold IRA exists when you need to withdraw funds before reaching 59 and a half years old. If you want to use that money right away however you need to consult a tax advisor.

If you do so you will likely owe income taxes on the funds.

In addition, rolling withdrawals will trigger an additional 10% if you are under the age of 59 and a half years old. This is an important factor when making a withdrawal decision.

Storing up Metals In IRAs.

If you’re planning to hold precious metals in IRAs, you should know that there are tax implications in the practice.

The IRS prohibits individuals from acting as custodians or trustees on their own retirement accounts. So storing precious metals under your mattress is out of the question.

Similarly, you cannot store precious metals linked to an IRA in a self-storage facility since it would be considered a distribution.

Depending on the metals you plan to hold, you need to store them in accordance with the IRA rules.

IRAs require metals to be stored in a bank. broker-dealers and third party administrators cannot store precious metals owned by IRAs.

Likewise, IRA´s owned LLCs must follow the same rules for storage. The custodian should be aware of the storage rules before recommending a custodian.

Another benefit of precious metals is that they are a safe asset. Your gold IRAs can protect your investments from high inflation and market volatility. By keeping your metals in an IRA, you can avoid the fees and storage costs that come with storing precious metals in a bank.

If you’re planning to buy gold or silver coins in your IRA, make sure you consult an IRA account executive. For additional details. You can also request a free precious metals information kit from them. Another issue to consider when storing your precious metals in an IRA is whether you can store them at home.

In the case of Donna Mc Nelton, she opened a separate bank account in the name of the LLC and documented a purchase of the coins. She then labeled them as property of her IRA-owned LLC and stored the coins at home. Safe-keeping precious metals at home is against IRS rules.

Contribution limits

Traditional gold IRAs are tax-deferred retirement saving accounts. Contributions to these accounts are tax-deferred, while the gains are not. The IRS has set contribution limits of $5,500 for individuals under age 50 and $6,500 for those over the age of 50.

Unlike IRA contributions to traditional gold IRAs, they are deductable for taxes. However, you must pay taxes on any distribution during your retirement.

To take advantage of these tax perks. You need a purchase go to a reputable custodian. Your custodian must be an IRA IRS-endorsed depository.

The custodian will keep your gold at a secure location as long as you hold the account. The IRS does not permit you to store the precious metals in your own home. However, you can sell or deliver the gold to your beneficiaries upon reaching retirement age. However, you cannot take possession of your gold assets unless you reach this age.

Individuals with a modified AGI below 125,000 They are going to be modified within AGI is over 140,000 and they may have a partial deduction. If you’re married filing separately, you may not take any deduction. This rule is not a hardship, but it is important to keep in mind and read the fine print.

This way, you will have the best chance of maximizing your gold ira tax benefits. So invest your money wisely and enjoy the tax benefits.

Rollover options

If you have some savings in a traditional IRA, you may be interested in a gold IRA rollover this option of global touch. Set an inherited tax rules apply to all types of IRAs and Roth IRA funds is tax deferred investing in gold is a great way to diversify your retirement and direct rollovers are never option. These rollovers are less attractive and direct rollovers. Rollovers are a little bit different since the plan administers liquidates your holdings and sends you a check. Then they withhold 20% or more of demonetised taxes, which they send to the IRS. After you deposit the full amount of the rollover damaged returns the extra 20% to you. This option isn’t as popular as a direct rollover, but it’s a convenient alternative for those with gold IRAs. There are many benefits to rolling over a gold IRA. The tax rules for the transaction are straightforward while you can withdraw money from a tax deferred account, you have to pay income tax and an exercise. If you’re under 59 and a half years old, the rollover of gold IRAs is tax free, as long as you complete the transaction within 60 days, however, you have to pay taxes on the amount you withdraw after 60 days. Another advantage to gold IRAs is that you can include physical acids to your retirement portfolio. Traditional IRAs can only hold stocks, bonds, or stocks. But the Taxpayer Relief Act of 1997 broaden IRA Investments precious metals can be included in a gold IRA self directed gold IRAs are also called alternative asset IRAs, but usually are only gold.